What Is an ACH Payment? Process, Types, Benefits, and Fraud Prevention

Author: Shashi Prakash Agarwal

Introduction

ACH payments are one of the most common ways money moves electronically between bank accounts in the United States. They power everyday financial activity such as direct deposit payroll, automatic bill payments, subscription charges, and bank-to-bank transfers. As more people manage their finances online, ACH has become a foundational payment rail for both consumers and businesses. Learning how ACH payments work, when they make sense, and how to protect yourself from fraud can help you manage cash flow more efficiently and avoid costly mistakes.

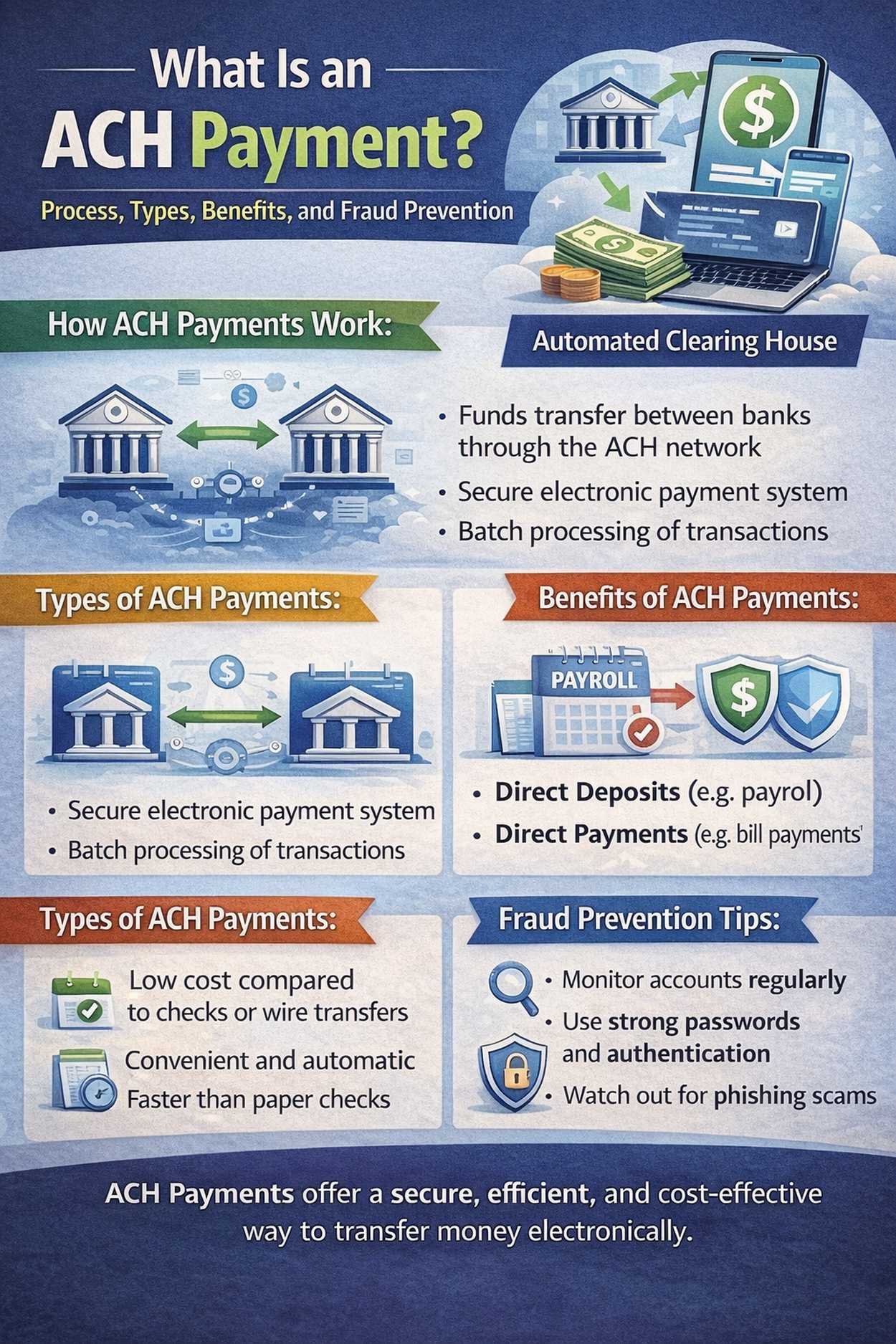

Understanding ACH Payments

ACH stands for Automated Clearing House, a network that processes electronic payments and bank transfers in batches. The ACH network is overseen by Nacha, an organization that sets operating rules and standards for participating financial institutions and payment providers. An ACH payment is an electronic funds transfer that moves money from one U.S. bank account to another using this network. Unlike card payments, which authorize and settle differently, ACH transfers rely on bank routing and account numbers and are processed through clearing and settlement cycles on business days. Although ACH processing runs frequently throughout the day, transfers usually do not settle instantly. Many ACH payments take anywhere from two to five business days to fully settle, depending on the banks involved, the type of transfer, and the timing of the transaction. Same-day ACH exists and is increasingly available, but standard ACH remains the most widely used option for routine transfers. ACH is heavily used for recurring payments. When customers authorize an organization to debit their account, the organization can automatically pull funds each month for services like utilities, loan payments, memberships, and subscriptions. ACH is also used for “push” transfers, such as salary direct deposits or transferring funds from a platform balance into a bank account.

NewTypes of ACH Payments Section

ACH transactions fall into two main categories: ACH credits and ACH debits. The difference comes down to who initiates the transfer and whether the payment is pushed or pulled. ACH credits are initiated by the payer. Money is pushed from the sender’s bank account into the recipient’s bank account. Payroll direct deposit is a classic example of an ACH credit, where an employer sends wages to employees’ accounts. ACH debits are initiated by the payee. Money is pulled from the payer’s bank account after the payer has authorized the arrangement. Automatic bill payments are the most familiar form of ACH debit, where a service provider withdraws payment from the customer’s account on scheduled dates. Understanding whether a payment is a credit or a debit is important because it affects control, timing, and how disputes may be handled if something goes wrong.

ACH Payments vs. Wire Transfers

ACH transfers and wire transfers both move money between bank accounts, but they are designed for different use cases. ACH payments are typically less expensive. Fees are often low, and in many cases businesses absorb the cost. Wire transfers commonly come with higher fees, especially when sent through banks. ACH payments can also be reversible in some situations, especially when a transaction is unauthorized or processed incorrectly and the dispute is raised in time. Wire transfers are generally harder to reverse once the funds have been sent and received, which makes wires riskier when the recipient is not fully trusted. Another advantage of ACH is flexibility. ACH can be set up for both push payments and pull payments, which supports common billing arrangements. Wire transfers are normally initiated by the sender only. The biggest drawback of ACH compared to wires is speed. Wire transfers can settle the same day or within hours depending on the bank and cut-off times. ACH often takes longer to settle, especially for standard transfers. ACH transfers are also usually domestic, while wire transfers can be domestic or international. For large one-time payments, such as real estate or high-value purchases, wires are still commonly used due to speed and higher transfer limits.

ACH Payment Fraud and How to Prevent It

ACH payments are generally safer than paper checks and can reduce risks associated with card skimming. However, fraud can still occur, especially through deception rather than technical hacking. Many ACH scams begin with fake invoices or urgent payment requests delivered through email, phone calls, or messaging. Fraudsters may impersonate legitimate companies, vendors, or even internal employees, pressuring targets to share bank information or authorize a transfer. To reduce the risk of ACH fraud, verify payment requests before acting, especially if they involve changes to bank details or unusual urgency. Confirm requests through official channels rather than replying to the message itself. Using two-factor authentication on banking and payment accounts adds a strong layer of protection. Monitoring account activity regularly and enabling alerts for withdrawals can help you detect suspicious transfers early. For businesses, tighter controls such as approval workflows, vendor verification steps, and bank account validation procedures can significantly reduce exposure to fraud.

Final Thoughts

ACH payments are a core part of modern banking because they make it easy to automate routine financial activity, reduce transaction costs, and move money electronically without relying on cards or cash. They work best for payroll, recurring bills, and everyday bank transfers where ultra-fast settlement is not essential. At the same time, ACH payments require careful handling of banking details and smart fraud prevention habits. With the right safeguards, ACH can be one of the most reliable and efficient payment methods for both consumers and businesses.